China’s solar panel industry is losing money

How manufacturing overcapacity halved China's solar export revenue and pushed its four biggest makers into the red.

China is the leader in producing solar panels at scale. In 2025, they installed 378 GW of new solar power capacity, compared with 242 GW across all other countries combined, according to data from Ember. That’s 61% of all the new solar capacity added globally.

In addition, China’s total solar panel exports reached a record 248 GW in 2025, which is actually more than the rest of the world installed that year. We can conclude that the vast majority of solar panels are produced in China and that they dominate the solar industry.

Given these numbers, you’d expect solar panels to generate a lot of revenue for Chinese manufacturers, but as we will see, that’s not the case.

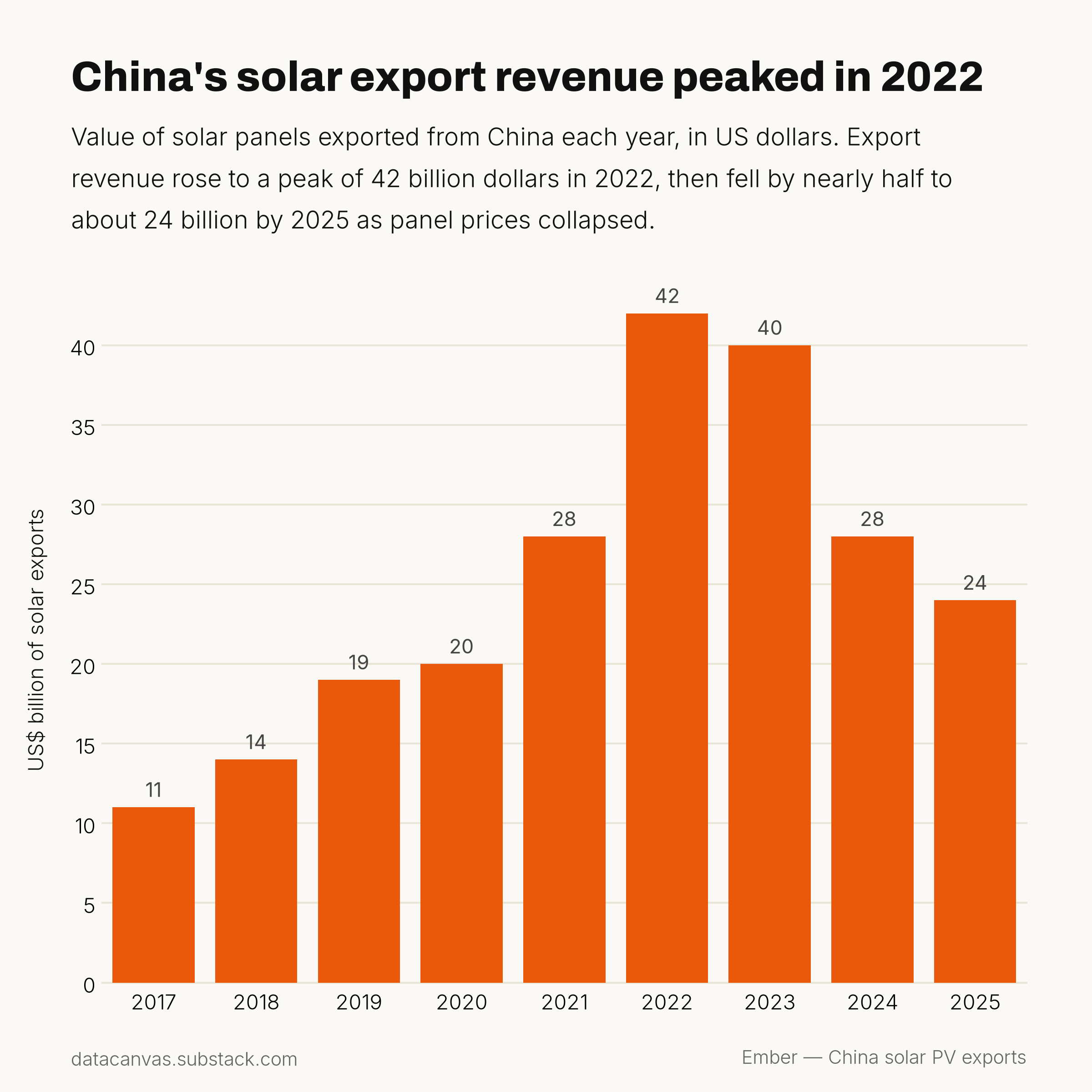

China’s revenue from solar panel exports peaked back in 2022 and has decreased ever since

China’s revenue from solar panel exports peaked in 2022 at $42.3 billion, following several years of steady growth. We first saw a small decrease in 2023, followed by a partial collapse in 2024. In 2025, revenue was down to $23.7 billion, a 44% drop in just three years.

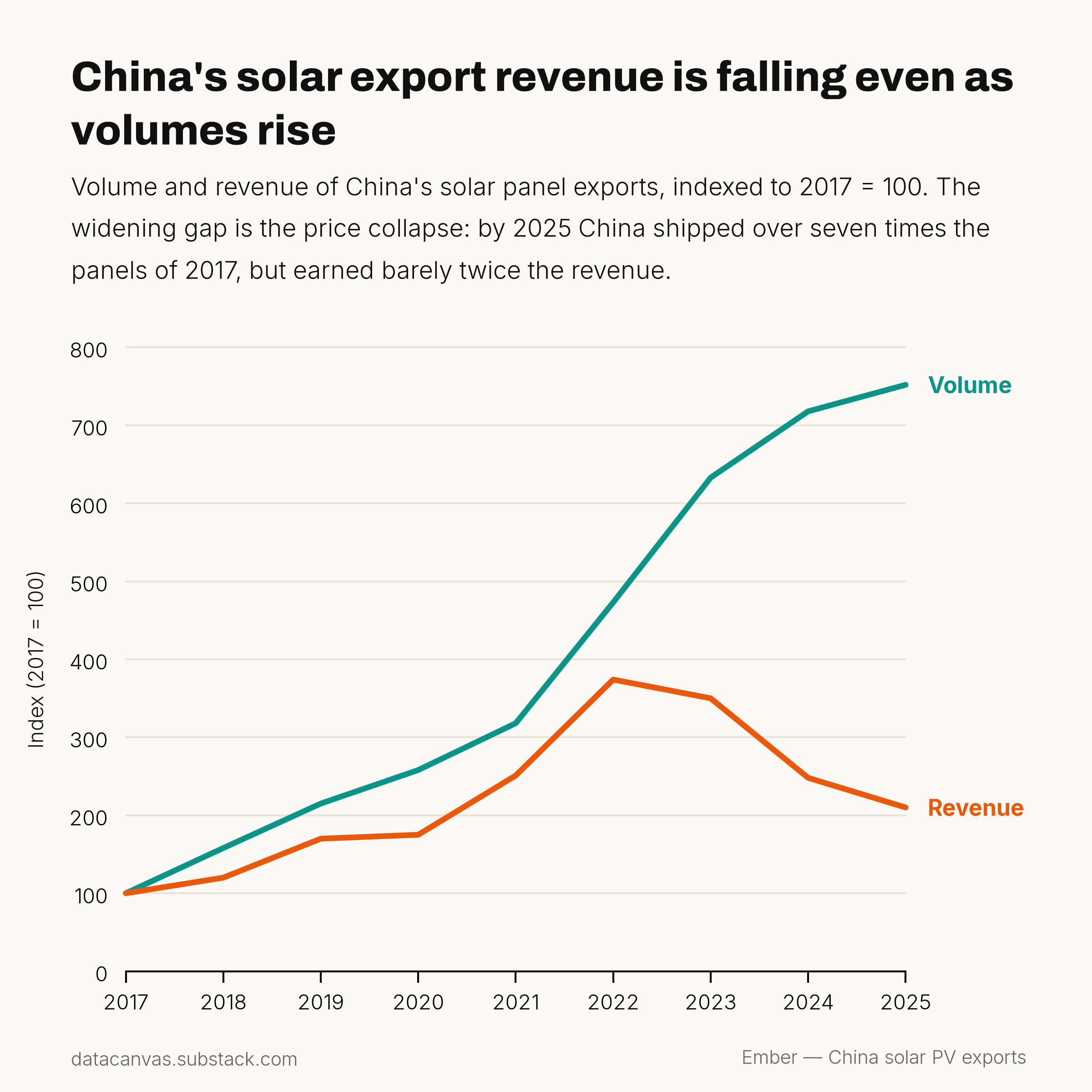

But the decline in revenue was not caused by a sudden lack of global demand; quite the opposite. The amount of exported GW has increased every year, and solar is by far the fastest-growing source of electricity generation. In other words, demand is not the problem, as you can see in the following table:

If we plot these values in relation to 2017, we see the pattern clearly. Volume increased dramatically in 2022, and revenue followed. But then, in 2023, revenue suddenly dropped, breaking the pattern from previous years.

The steady increase in demand triggered a building frenzy as manufacturers expanded their capacity, thinking demand would follow. By 2024, China’s module-making capacity had reached 1,100+ GW per year1.

But demand didn’t rise as quickly as capacity, and Chinese manufacturers now produced far more solar panels than the World wanted to purchase.

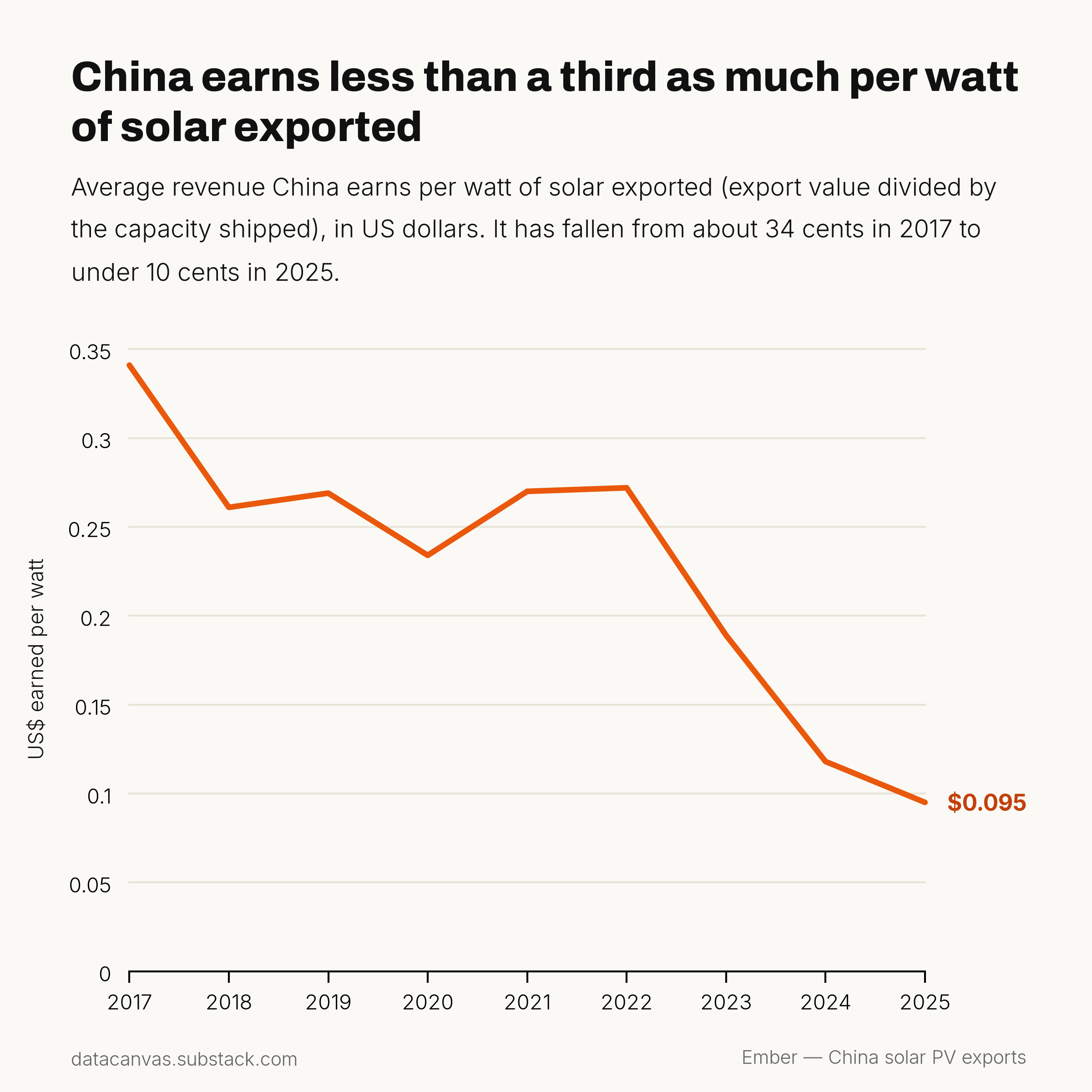

It’s true that the cost of solar panels has decreased over time due to technological advances. But the sudden price drop that led to a decline in export revenues stemmed from manufacturing overcapacity.

After a period of relatively stable prices, the average revenue per watt went from $0.27 in 2022 to $0.095 in 2025.

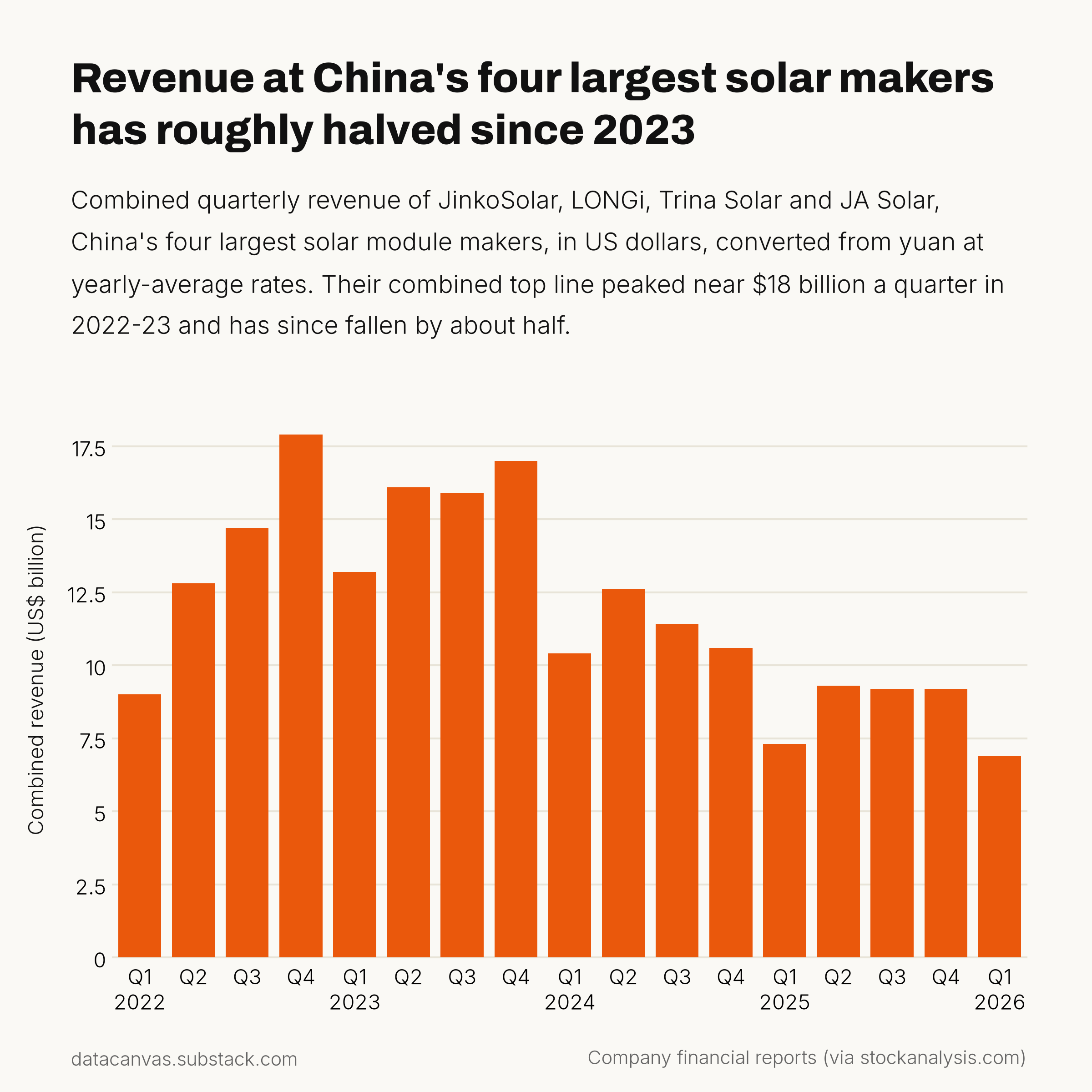

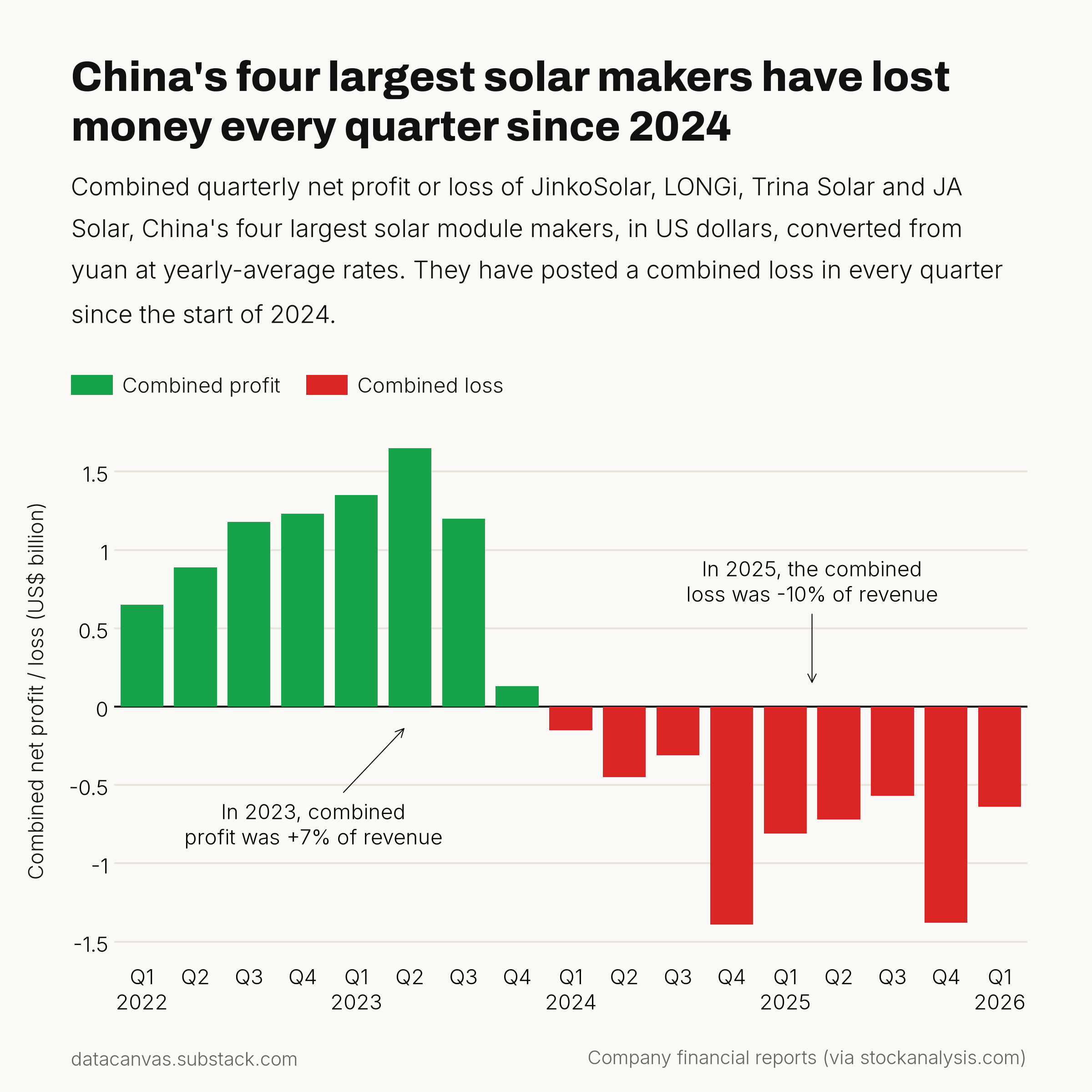

None of the large manufacturers managed to keep their numbers green as the price for their goods collapsed.

Exploring numbers for China’s largest vertically-integrated module manufacturers

Vertically-integrated module manufacturers are companies that produce wafers, cells, and finished solar panels. The four largest such companies in China are JinkoSolar, LONGi, Trina Solar, and JA Solar. Each one was founded by entrepreneurs (and is not state-owned) and is now publicly traded on Chinese stock exchanges.

Looking at their quarterly revenues, we see the same pattern we saw in the export data. In 2022 and 2023, the combined revenue hovered around $15B compared to less than $10B every quarter since the start of 2025.

Again, they produced and delivered more solar panels than ever before, but at a lower price point. The effect is even more striking if we instead look at their combined profits, where there’s a clear shift from green to red values in 2024.

A booming business suddenly turns completely red over a few months as demand increases more slowly compared to capacity. Solar might be the fastest-growing source of electricity, but it’s not growing as quickly as these companies thought it would.

So where do Chinese solar panels end up, and who is the primary customer?

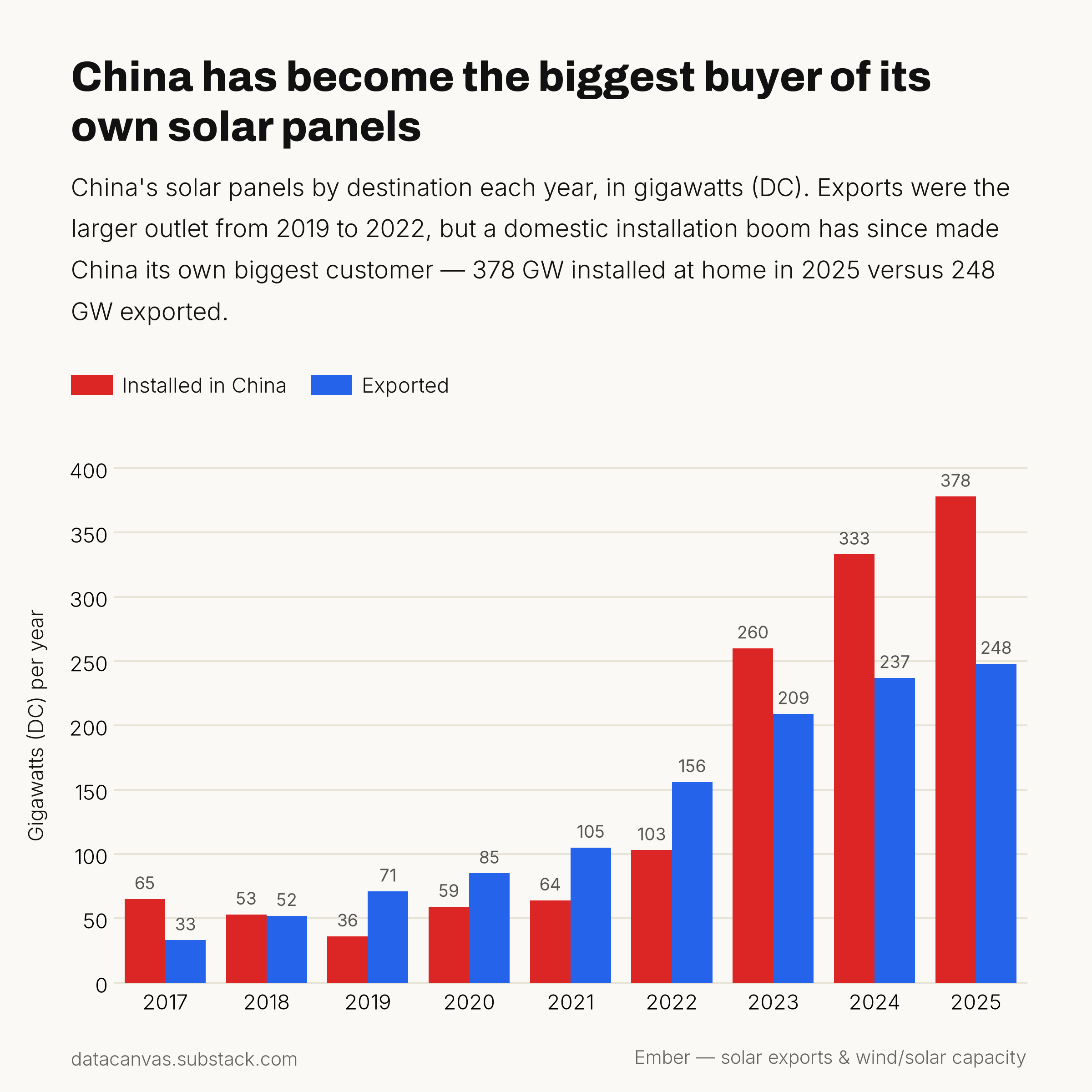

As mentioned in the introduction, most solar panels produced by Chinese manufacturers don’t end up on a ship. Before the building frenzy started, most solar panels were exported to other countries, but in 2023, China itself became the largest customer, and that hasn’t changed since.

In 2023, 2024, and 2025, China installed more solar capacity at home than it exported to the rest of the world, and the gap has widened.

Perhaps Chinese manufacturers knew about the increased demand from their own government and thought the same patterns would repeat for their other customers. We can clearly see that exports increase far more slowly than domestic installations and even seem to stagnate year by year.

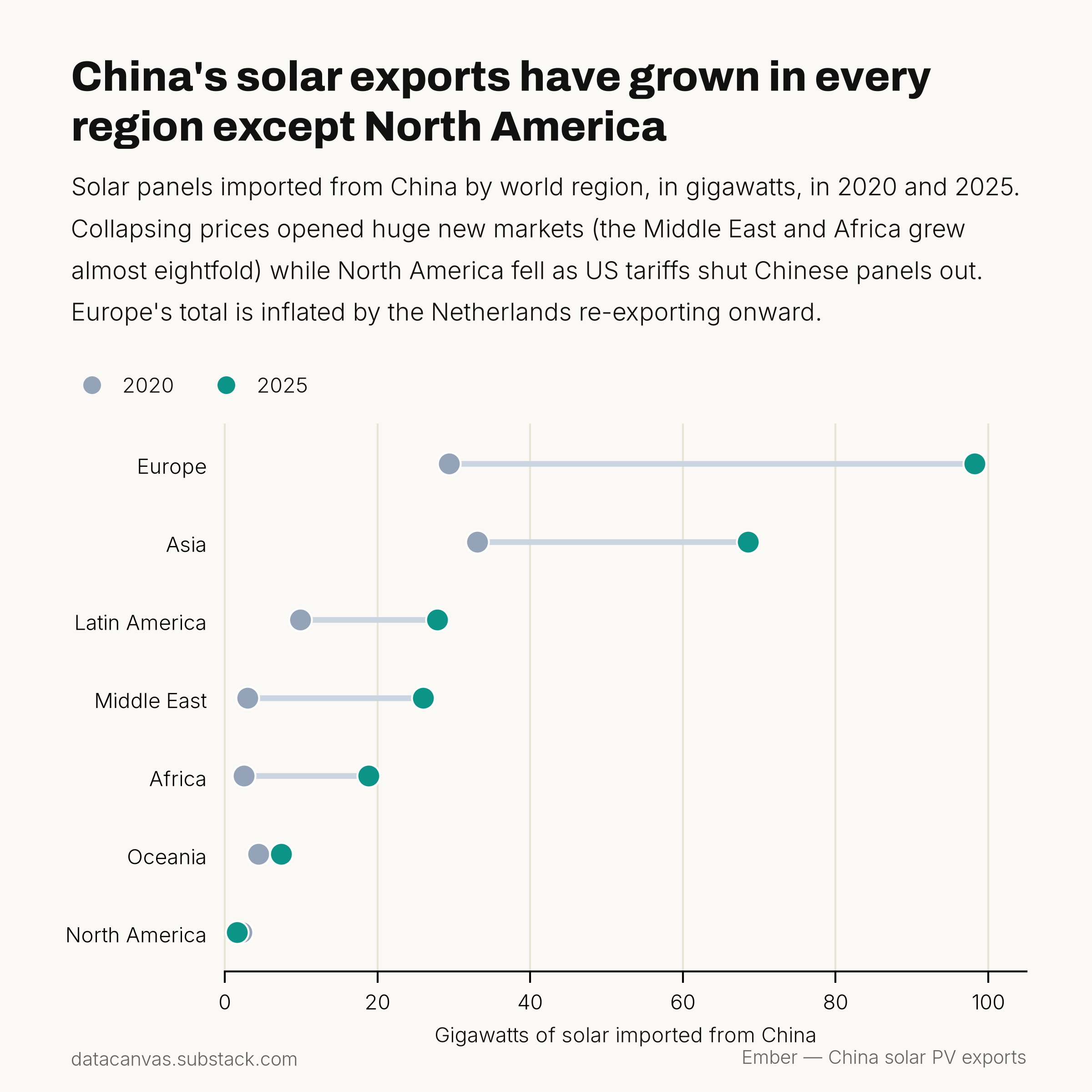

Still, large numbers of solar panels are exported to other countries, with Europe and Asia remaining the largest markets.

Perhaps Africa and the Middle East can make solar exports boom again. In just five years, exports to these locations grew by more than 700% and it wouldn’t be surprising if that demand continued to increase. Solar power is a fantastic source of electricity for poor nations because it’s cheap and easy to install locally when you don’t have stable grids. But it’s hard to imagine that these nations can generate enough demand to absorb for the current overcapacity.

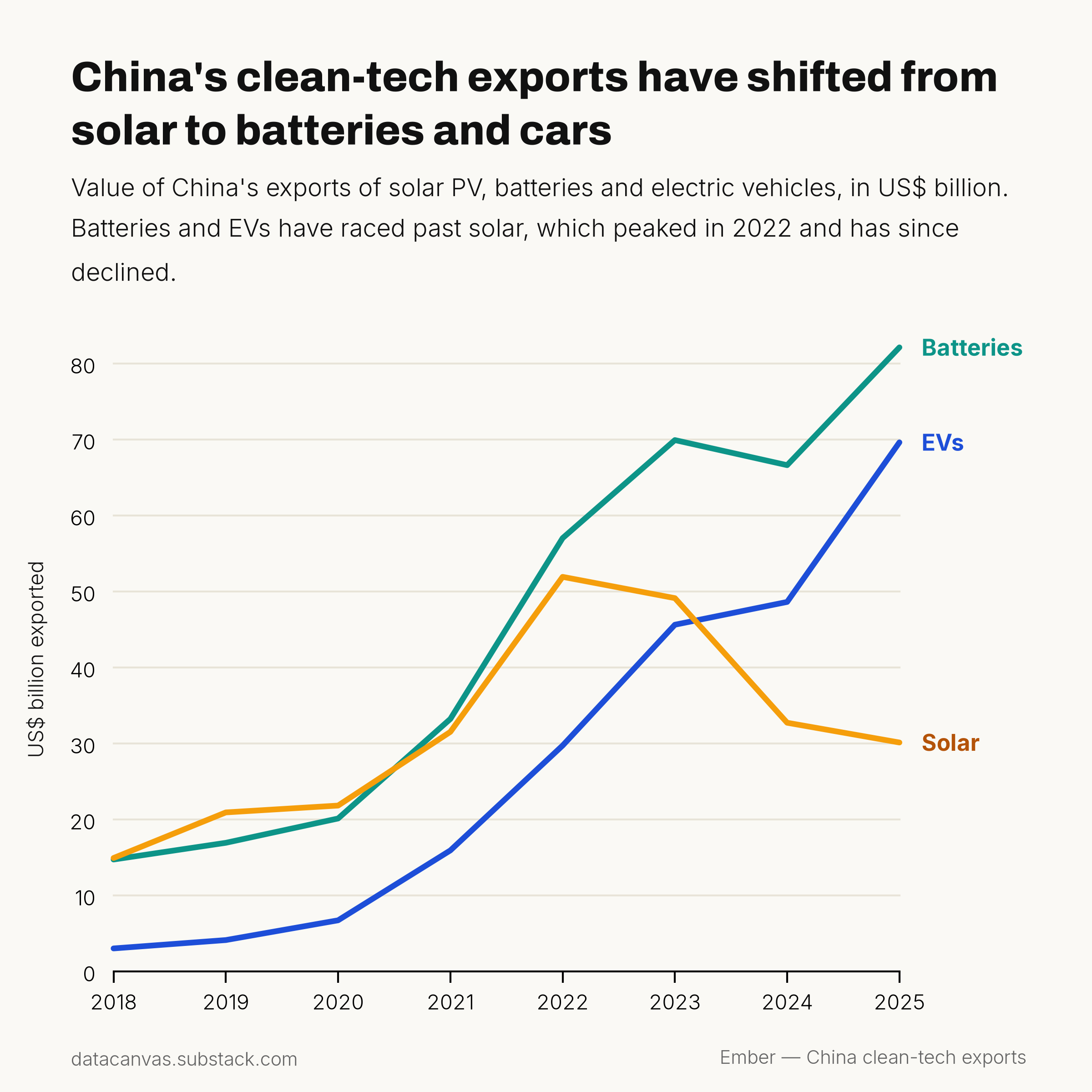

Does this mean that Chinese clean tech exports are decreasing overall?

China is in a better position than any other country to become the global leader in any type of clean tech. They refine most of the critical minerals, from cobalt mined in Congo to lithium mined in Australia or Chile. Not to mention several rare earths for which they practically have a monopoly on refining.

So while solar doesn’t look like a promising investment any longer, batteries and EVs more than make up for it, but that’s for another article.

Note that the solar PV includes panel, cells, and wafers while the first chart in this article only include panels.

Summary & Thank you

Solar panels looked like a promising industry as demand increased quickly. Chinese manufacturers invested too heavily in production capacity, which led to a significant drop in prices. Revenue has decreased ever since even though volumes keep going up. Right now, it’s difficult to see manufacturing of solar panels becoming a booming business yet.

Thank you for reading, and don’t hesitate to ask your questions and provide feedback.

"Overcapacity" for how long, exactly? It's not at all difficult to make a case for 15-20TWp global installed capacity c. 2040, suggesting something along the lines of 1 to 1.5 TWp demand per year (on average) over the next 15 years, conservatively. We also know from recent losses/revenue ratios that the big Chinese PV majors have driven their COGS to 9.5 to 10.5 cents per Watt, which is about half that of their artisanal Western "balanced capacity" competitors. If the Chinese majors are right that demand will eventually catch up with supply, who do you think prevails in that scenario: high-volume/low cost/low margin, or trickle-volume/high cost/high margin? What kind of providers prevailed historically when it came to coal, oil, gas,or hydro energy capacity? Given how critical PV/EV/ESS tech is to most of the world's long-term economic and security interests, the overcapacity crowd sounds a lot like the people who were finger-wagging the overcapacity of oil wells in 1910, digital calculators in 1975, data fibre in 1999, or high-speed rail in 2015. Same pattern as before with zero lessons learned, apparently.